.svg)

What does it mean when your car is written off?

A car is considered a write-off (total loss) when your insurer decides that:

- The cost of repairs is too high compared to the car’s value, or

- The vehicle is too damaged to be safely repaired

Instead of repairing it, your insurer will offer a cash settlement based on its market value before the incident.

Step 1: Your insurer assesses the damage

After an accident, theft, or damage:

- Your insurer inspects the vehicle (or reviews images/report)

- They estimate repair costs

- They compare this to the car’s value

👉 If repairs are uneconomical, the car is declared a total loss.

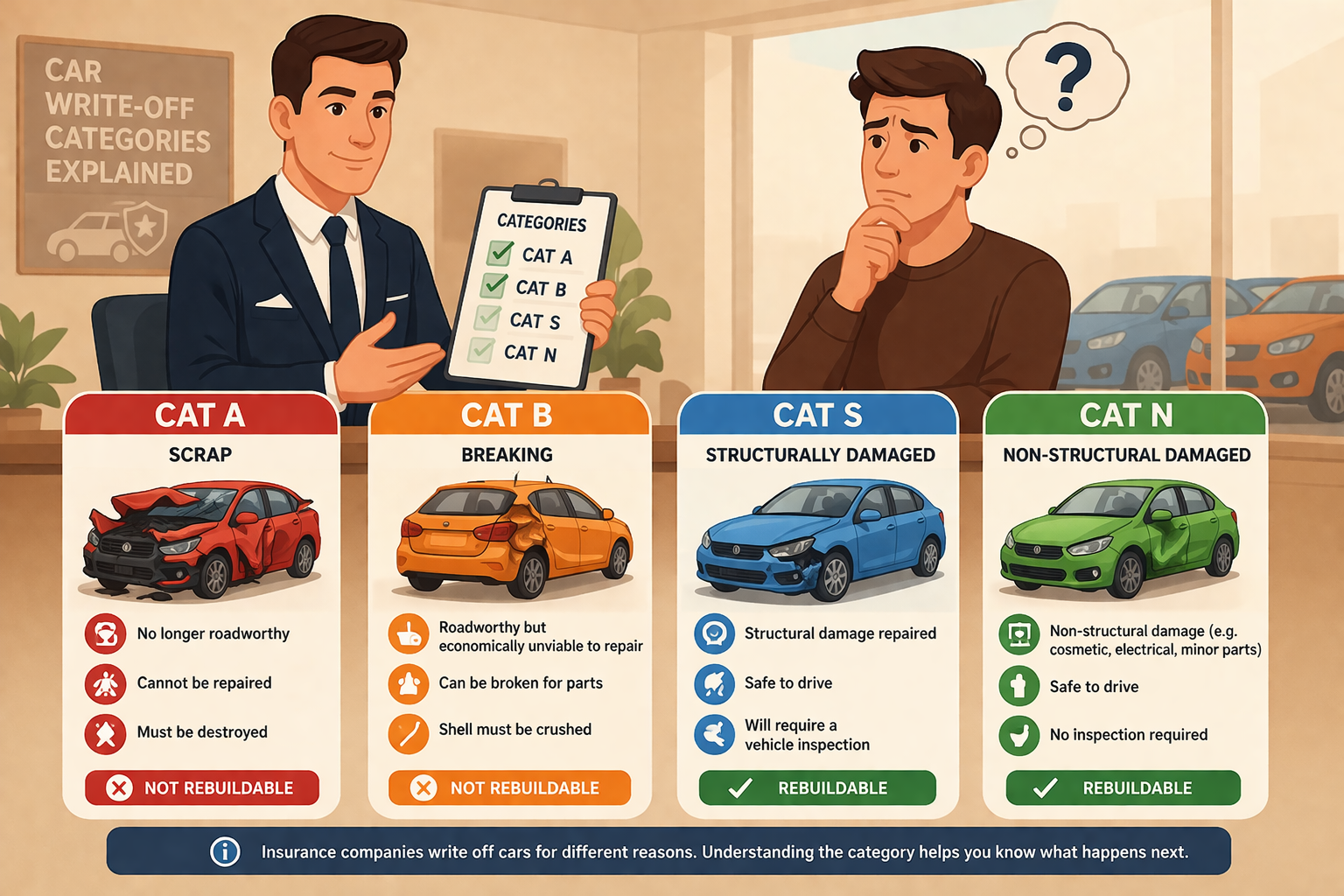

Step 2: Your car is assigned a write-off category

Your vehicle will be placed into one of these categories:

- Category A – Must be scrapped entirely

- Category B – Parts can be salvaged, shell destroyed

- Category S – Structural damage, repairable

- Category N – Non-structural damage

👉 This classification affects whether the car can return to the road and its future value.

Step 3: You receive a settlement offer

Your insurer will offer a payout based on the car’s pre-accident market value.

This is supposed to reflect what it would cost to buy a similar car just before the incident.

However, this is where problems often occur:

👉 Many drivers receive less than their car was actually worth.

Step 4: Check if the payout is fair

Before accepting the offer, you should:

- Search for similar vehicles on sites like AutoTrader

- Compare mileage, condition, and specification

- Check if you could realistically replace your car with the payout

👉 If you can’t find a like-for-like replacement, the valuation may be too low.

Step 5: Gather evidence (if needed)

If you believe the payout is undervalued, collect:

- Listings of similar vehicles

- Service history and condition details

- Receipts for upgrades or repairs

- Independent valuations (if available)

This strengthens your position when challenging the insurer.

Step 6: Challenge the valuation

You have the right to challenge your insurer’s offer.

You can:

- Contact your insurer and request a review

- Provide your supporting evidence

- Ask for a revised settlement

👉 Many insurers increase payouts when challenged.

Step 7: Escalate to the Financial Ombudsman (if needed)

If your insurer refuses to increase the offer:

- You can take your case to the Financial Ombudsman Service (FOS)

- This is free and independent

- They can order the insurer to increase your payout

👉 The Ombudsman regularly upholds complaints where cars were undervalued.

How long does the process take?

- Initial insurer response: up to 8 weeks

- Ombudsman review (if needed): several weeks to months

👉 Simple disputes can be resolved quickly, especially with strong evidence.

Can you keep your written-off car?

In some cases, yes.

If your car is:

- Category S or N, you may be able to buy it back from the insurer

However:

- The payout will be reduced

- The car may have a lower resale value

Common mistakes to avoid

❌ Accepting the first offer without checking

❌ Not comparing real market prices

❌ Assuming insurers always get valuations right

❌ Not knowing you can challenge the payout

👉 These mistakes can cost you hundreds or even thousands of pounds.

Key takeaway

👉 Your insurer’s first offer is not always the correct value.

If your car has been written off:

- You are entitled to a fair market value

- You can challenge the valuation

- You can escalate your complaint for free

Check if your payout was too low

If your car was written off and your settlement didn’t feel right, you could still be owed money.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today