.svg)

What are car write-off categories?

Write-off categories are used by insurers to classify the severity of damage to a vehicle.

They help determine:

- If the car is repairable

- If it can be safely used again

- How it should be disposed of

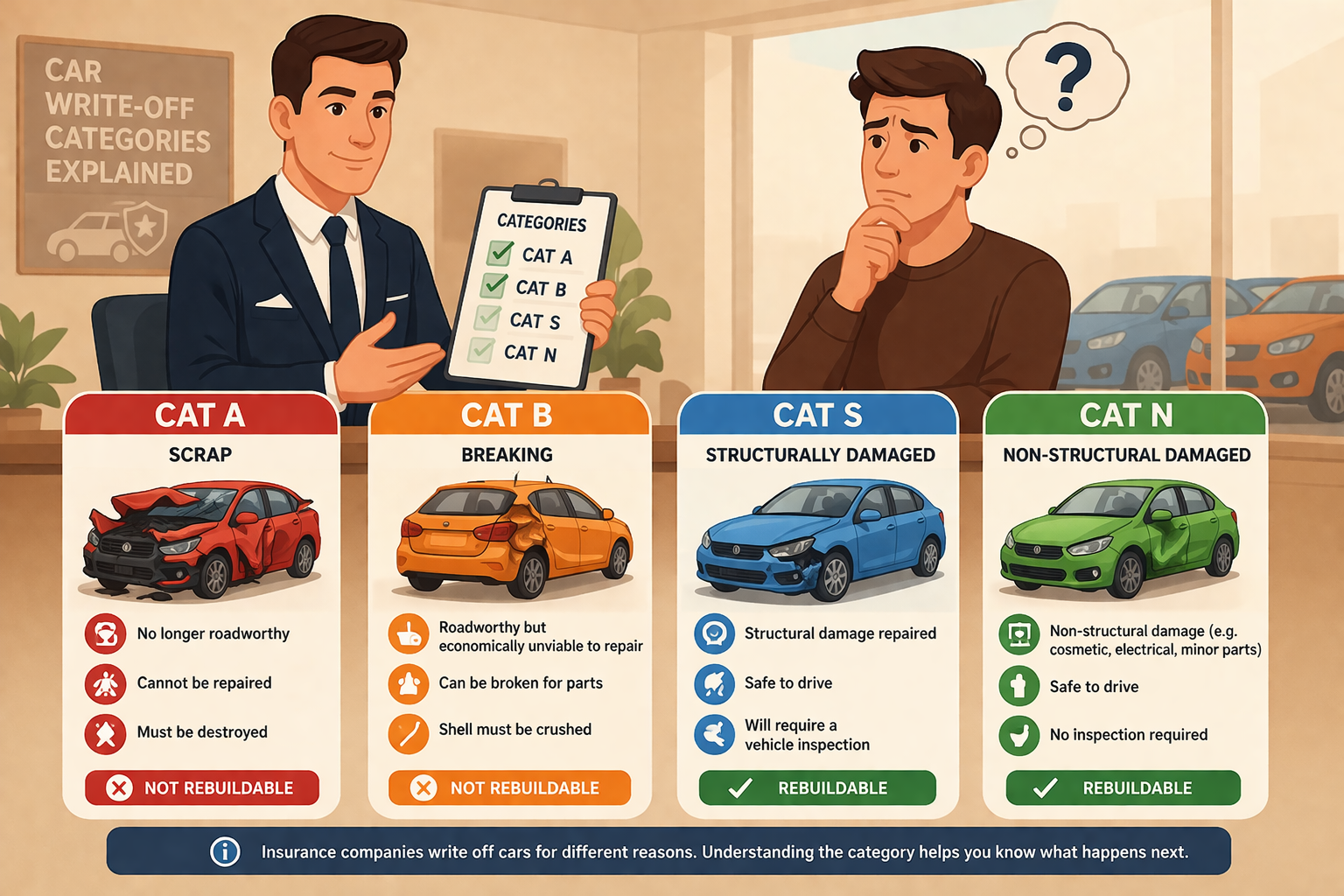

The four current write-off categories

Category A (Cat A) – Scrap only

- Vehicle is completely destroyed

- Cannot be repaired or reused

- Must be crushed entirely

👉 No parts can be salvaged.

Category B (Cat B) – Break for parts

- Severe damage

- Body shell must be destroyed

- Some parts can be salvaged

👉 The car itself will never return to the road.

Category S (Cat S) – Structural damage

- Damage to structural parts (e.g. chassis)

- Can be repaired professionally

- Can return to the road

👉 However, the vehicle’s value is usually reduced.

Category N (Cat N) – Non-structural damage

- No structural damage

- May include cosmetic or electrical issues

- Repairable and roadworthy after repair

👉 Often less serious than Cat S.

Old categories (Cat C and Cat D)

Before 2017, insurers used:

- Cat C → Now replaced by Cat S

- Cat D → Now replaced by Cat N

👉 You may still see these terms used for older vehicles.

How write-off categories affect your payout

Here’s the key point many drivers misunderstand:

👉 Your insurance payout is based on the car’s value BEFORE the accident — not its write-off category.

However:

- Severe damage may influence how insurers assess value

- Disputes can arise if valuations don’t reflect true market prices

Common confusion about categories

❌ “Cat S or N means lower payout”

✔ Not necessarily — payout should reflect pre-accident value

❌ “If it’s repairable, it shouldn’t be written off”

✔ Write-offs are based on cost vs value, not just repairability

❌ “The category decides what I’m paid”

✔ The key factor is market value before the incident

Can you keep a written-off car?

In some cases, yes.

If your car is:

- Category S or N, you may be able to buy it back

However:

- Your payout will be reduced

- The car may have lower resale value

How categories affect future value

If a car is repaired and returned to the road:

- Cat S vehicles → Typically lose more value

- Cat N vehicles → Less impact but still recorded

👉 Buyers and insurers will see this history.

What if you disagree with the write-off decision?

You can challenge:

- The valuation of your vehicle

- The insurance payout offered

👉 Even if the category is correct, the payout may still be too low.

Key takeaway

👉 Write-off categories describe the damage — not what you’re entitled to.

If your car has been written off:

- Your payout should reflect its true market value before the incident

- You can challenge the valuation if it’s too low

- The category does not limit your right to a fair settlement

Check if your payout was too low

If your car was written off and your settlement didn’t reflect its true value, you could still be owed money.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today