.svg)

Step 1: Your complaint is acknowledged

Once you submit a complaint:

- Your insurer will confirm receipt

- Your case is logged internally

- A handler is assigned to review it

👉 This usually happens within a few days.

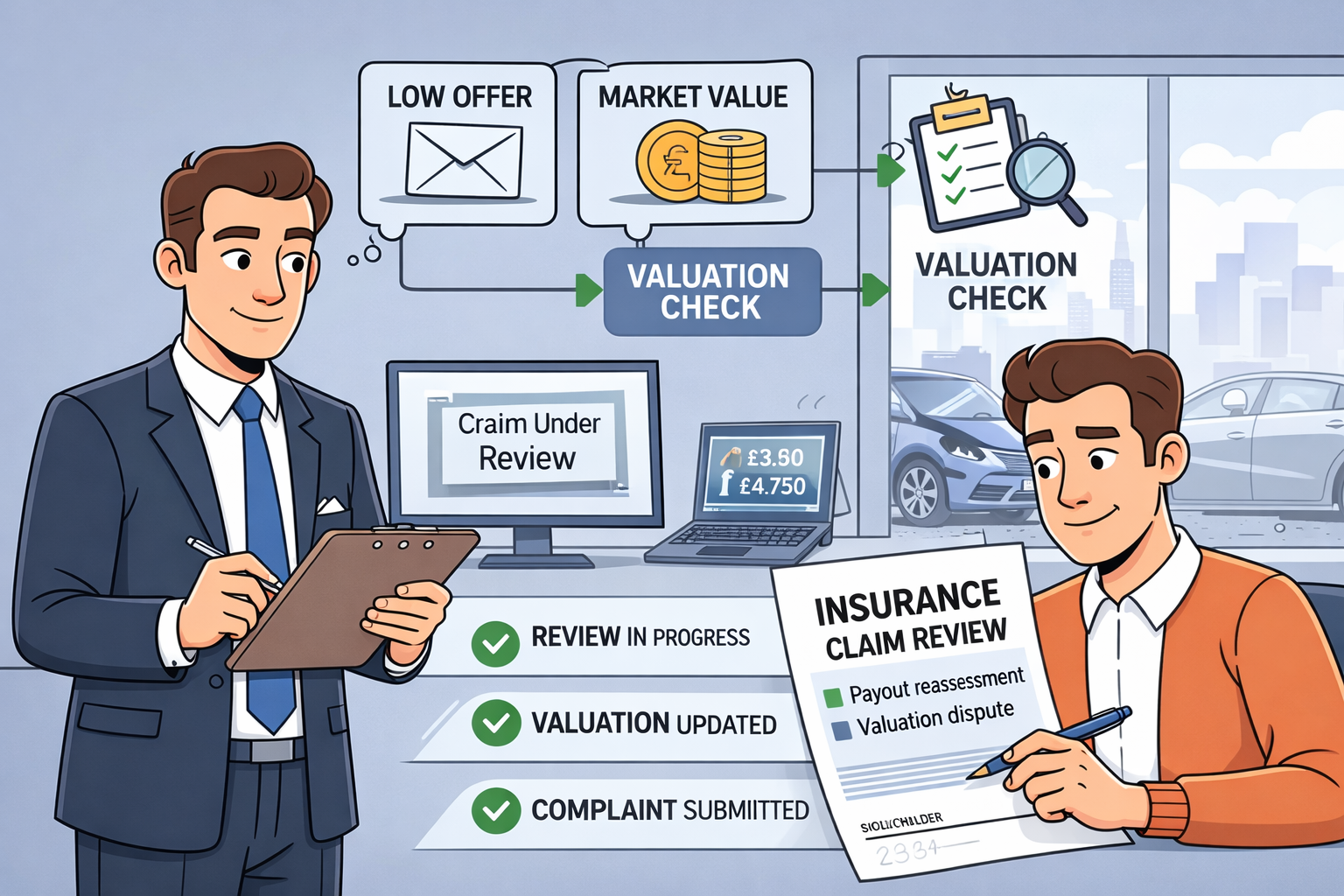

Step 2: The insurer reviews your claim

At this stage, the insurer will:

- Reassess your vehicle valuation

- Review any evidence you’ve provided

- Compare additional market data

👉 This is the key opportunity for your payout to increase.

Step 3: You may receive a revised offer

After reviewing your case, the insurer may:

- ✔ Increase your payout

- ✔ Partially adjust the valuation

- ❌ Reject your complaint

👉 Many drivers receive higher offers at this stage, especially with strong evidence.

Step 4: Final response (within 8 weeks)

By law, insurers must issue a final response within:

👉 Up to 8 weeks

This will explain:

- Their decision

- Whether they accept your complaint

- Any revised settlement offered

Step 5: Escalation to the Financial Ombudsman

If you’re not satisfied:

- You can take your case to the Financial Ombudsman Service (FOS)

- This is free and independent

- They will review both sides and make a binding decision

👉 The Ombudsman often upholds complaints where valuations are too low.

What most drivers don’t realise

Many people stop after the insurer says no.

But in reality:

👉 Some of the biggest increases happen after escalation.

Drivers who persist often recover:

- £500–£1,000 (common)

- £1,000–£3,000 (typical disputes)

- £3,000+ (strong cases)

Where things can go wrong

Challenging a payout isn’t always straightforward.

Common issues include:

- Weak or limited evidence

- Poor-quality comparisons

- Insurers rejecting claims due to lack of detail

- Giving up too early

👉 This is where outcomes can vary significantly.

Why many drivers choose expert help at this stage

While you can handle the process yourself, many people choose support after submitting a complaint — especially if:

Their claim has been rejected

A specialist can rebuild the case with stronger evidence

They want a stronger challenge

Structured, professional submissions often carry more weight

They don’t want the hassle

Back-and-forth with insurers can be time-consuming

They want to maximise their payout

Well-prepared claims often achieve better outcomes

DIY vs expert support — what’s the difference?

✔ Doing it yourself

- Free

- Full control

- Requires time and research

✔ Using a claims management company

- No upfront cost (typically No Win, No Fee)

- Full case handling

- Professional valuation evidence

- Escalation handled for you

👉 For many drivers, it’s the difference between:

- Accepting a small increase

- Or recovering the full amount they’re owed

Is it too late to challenge your payout?

No — in many cases, you can still act even if:

- You’ve already accepted the payout

- The claim was settled months or years ago

👉 Time limits usually apply (up to 6 years in many cases).

Key takeaway

👉 Challenging your payout is often where the real outcome is decided.

What happens next depends on:

- The strength of your evidence

- How the case is presented

- Whether you escalate if needed

Check if your payout could be increased

If your car was written off and your payout felt too low, you could still recover more.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today

Important note

You can complain directly to your insurer and refer your case to the Financial Ombudsman Service for free.