.svg)

Step 1: Report the incident to your insurer

As soon as possible:

- Contact your insurer

- Provide details of the accident, theft, or damage

- Submit photos if requested

👉 This officially starts your claim and allows the insurer to begin assessing your vehicle.

Step 2: Provide key information

Your insurer will ask for:

- Vehicle registration

- Policy details

- Description of the incident

- Date and location

👉 Providing accurate information helps prevent delays later in the process.

Step 3: Vehicle assessment and write-off decision

The insurer will:

- Inspect the vehicle (or review images/reports)

- Estimate repair costs

- Decide whether the car is repairable

If repairs are uneconomical, your vehicle will be declared a total loss (write-off).

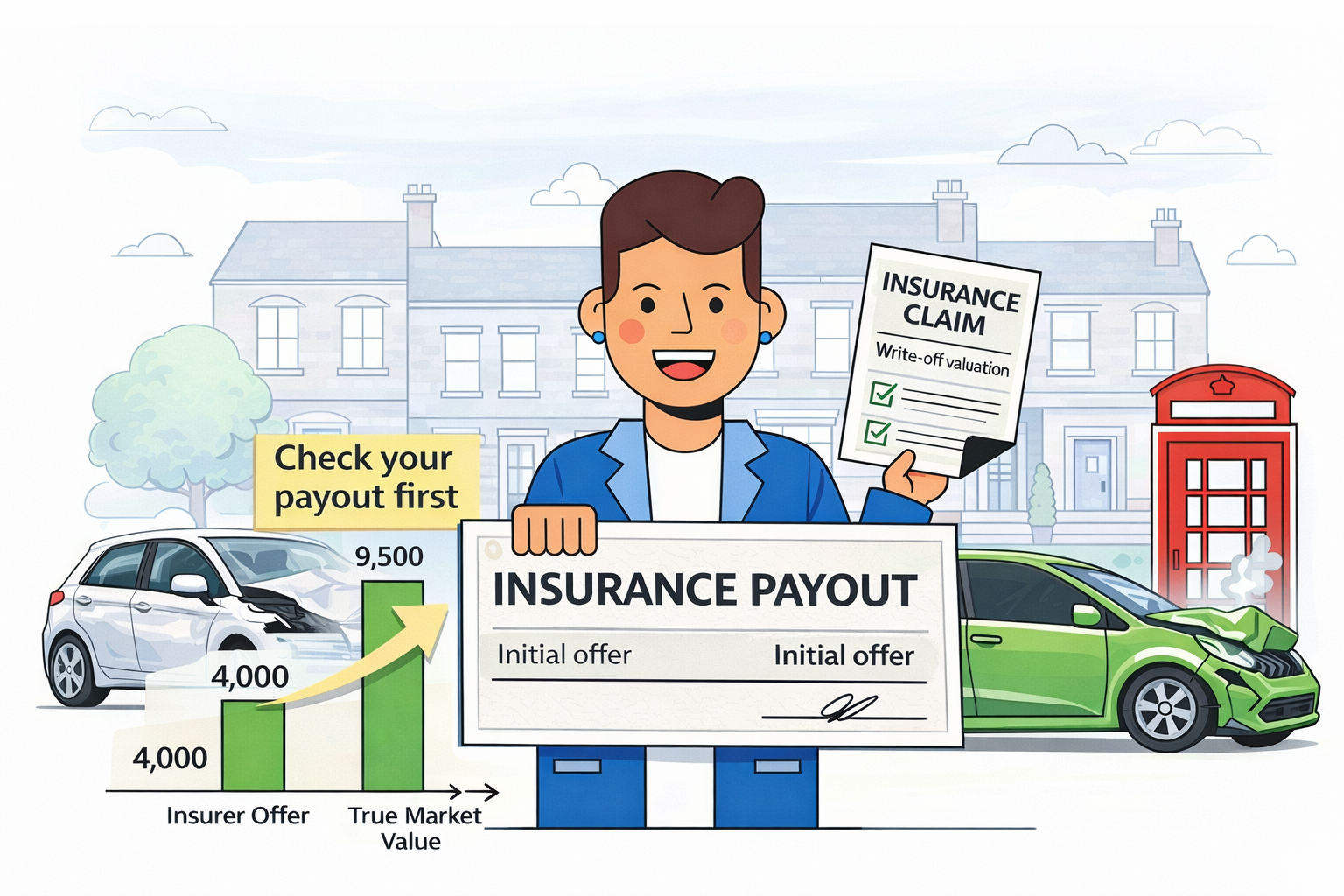

Step 4: Receive your settlement offer

Once your car is written off, your insurer will offer a payout based on its market value before the incident.

👉 This is the most important stage of the process — and where many drivers lose money.

Step 5: Don’t accept the first offer without checking

Before accepting:

- Compare similar vehicles for sale online

- Check mileage, condition, and specification

- Ask yourself: Could I replace my car with this amount?

👉 If the answer is no, your payout may be too low.

Why many drivers are underpaid

Insurance valuations are not always accurate.

Common issues include:

- Using trade values instead of retail prices

- Comparing with cheaper or non-equivalent vehicles

- Ignoring condition, history, or upgrades

- Relying on outdated pricing data

👉 This can leave drivers hundreds or even thousands of pounds out of pocket.

Your options: claim yourself or get expert help

At this stage, you have two choices:

Option 1: Handle the claim yourself (free)

You can:

- Challenge the valuation

- Provide your own evidence

- Escalate to the Financial Ombudsman if needed

👉 This costs nothing, but requires time, research, and confidence.

Option 2: Use a claims management company

A specialist can:

- Review your original payout

- Identify if your car was undervalued

- Gather professional valuation evidence

- Handle all communication with your insurer

- Escalate your claim if needed

👉 Many drivers choose this route to maximise their payout and reduce stress.

Why people choose professional support

While it’s possible to claim yourself, many drivers prefer expert help because:

Better evidence

Specialists use valuation tools and market data most drivers don’t have access to

Stronger negotiation

Insurers are more likely to revise offers when presented with structured, professional evidence

Time-saving

The entire process is handled for you

Higher potential outcomes

Claims are often worth more when properly challenged

Is it worth getting help for a write-off claim?

If your payout feels too low, the answer is often yes.

Even small differences can matter:

- £500–£1,000 → common undervaluation

- £1,000–£3,000 → typical dispute range

- £3,000+ → more complex cases

👉 The key question is: how confident are you challenging it yourself?

Important: you don’t have to use a claims company

You are always entitled to:

- Complain directly to your insurer

- Refer your case to the Financial Ombudsman Service for free

👉 However, some people choose support to improve their chances of success.

Key takeaway

👉 Starting your claim properly — and reviewing your payout carefully — can make a significant financial difference.

If your car has been written off:

- Don’t assume the first offer is correct

- Check the valuation properly

- Consider whether you want to handle the claim yourself or get support

Check if your payout was too low

If your car was written off and your settlement didn’t feel right, you could still be owed money.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today