.svg)

Case Reference: DRN-3016070

Outcome: Complaint upheld

Additional compensation awarded: £899

What happened in this case?

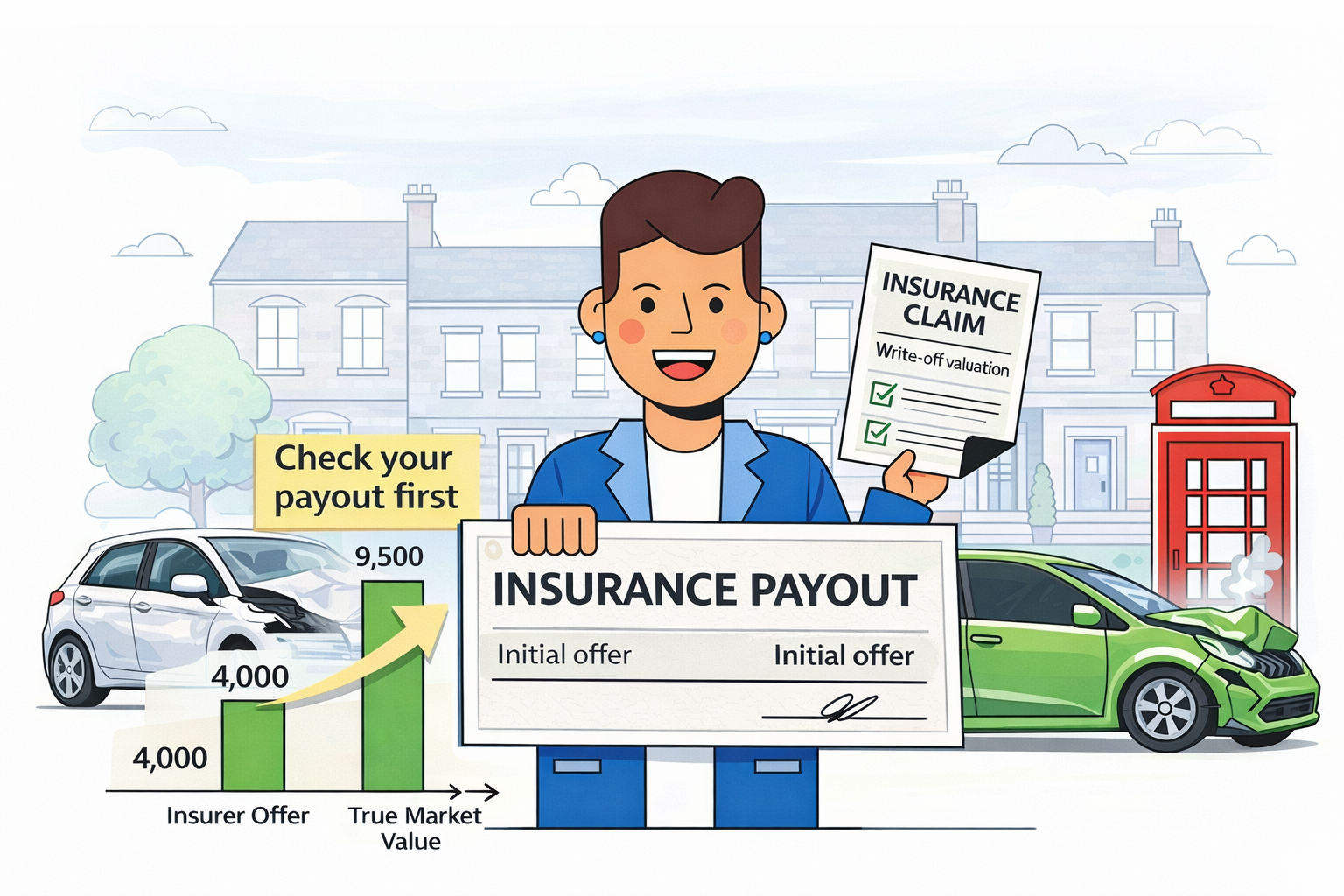

The customer’s vehicle was declared a total loss (write-off) following an incident.

Their insurer offered a settlement based on its estimated market value, which the customer initially received.

However, after reviewing the payout, the customer believed the amount was too low and did not reflect what it would actually cost to replace the vehicle.

The issue: a modest but unfair undervaluation

Unlike some high-value disputes, this case involved a smaller difference — but the principle was the same:

👉 The insurer’s valuation did not reflect the true market price of the vehicle.

The customer argued:

- The insurer relied on valuation tools that didn’t match real market listings

- Comparable vehicles were priced higher than the settlement offered

- The payout left them out of pocket when trying to replace the car

What did the Ombudsman review?

The Financial Ombudsman considered:

- Motor trade valuation guides

- Real-world listings of similar vehicles

- The vehicle’s condition, age, and mileage

- Whether the insurer’s evidence was fair and representative

The key test was simple:

👉 Would the payout allow the customer to buy a like-for-like replacement?

The Ombudsman’s decision

The complaint was upheld.

The Ombudsman found that:

- The insurer’s valuation was slightly but materially too low

- The evidence supported a higher market value

- The customer had been financially disadvantaged, even if the difference was under £1,000

The outcome

The insurer was instructed to:

- Pay an additional £899

- Adjust the settlement to reflect a fair market value

- Compensate the customer for the shortfall

Key takeaway from this case

👉 Even smaller undervaluations are worth challenging.

This case shows:

- You don’t need a £5,000+ dispute to have a valid claim

- The Ombudsman will act on fairness — not just large amounts

- Many drivers may be owed money without realising it

Why this matters for everyday drivers

Most write-off disputes fall into this range:

- £500 to £2,000 undervaluation

Because of this, many people:

- Don’t question the payout

- Assume it’s “not worth the hassle”

- Accept less than they’re entitled to

👉 But this case proves otherwise.

What should you do if your payout seems slightly low?

If your car was written off and the payout didn’t feel quite right:

- Check similar vehicles for sale online

- Compare prices with your settlement

- Raise a complaint with your insurer

- Escalate to the Financial Ombudsman if needed

👉 Even a small difference can be reclaimed.

Is it worth claiming for under £1,000?

Yes.

This case confirms:

- The Ombudsman will review smaller disputes

- Insurers must still pay a fair market value

- You are entitled to the full amount — not a “close enough” estimate

Check if you were underpaid

If your car was written off and your payout seemed low — even slightly — you could still recover the difference.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today

Important note

You can complain directly to your insurer and refer your case to the Financial Ombudsman Service for free.