.svg)

Case Reference: DRN-4660949

Outcome: Complaint upheld

Additional compensation awarded: Over £6,000

What happened in this case?

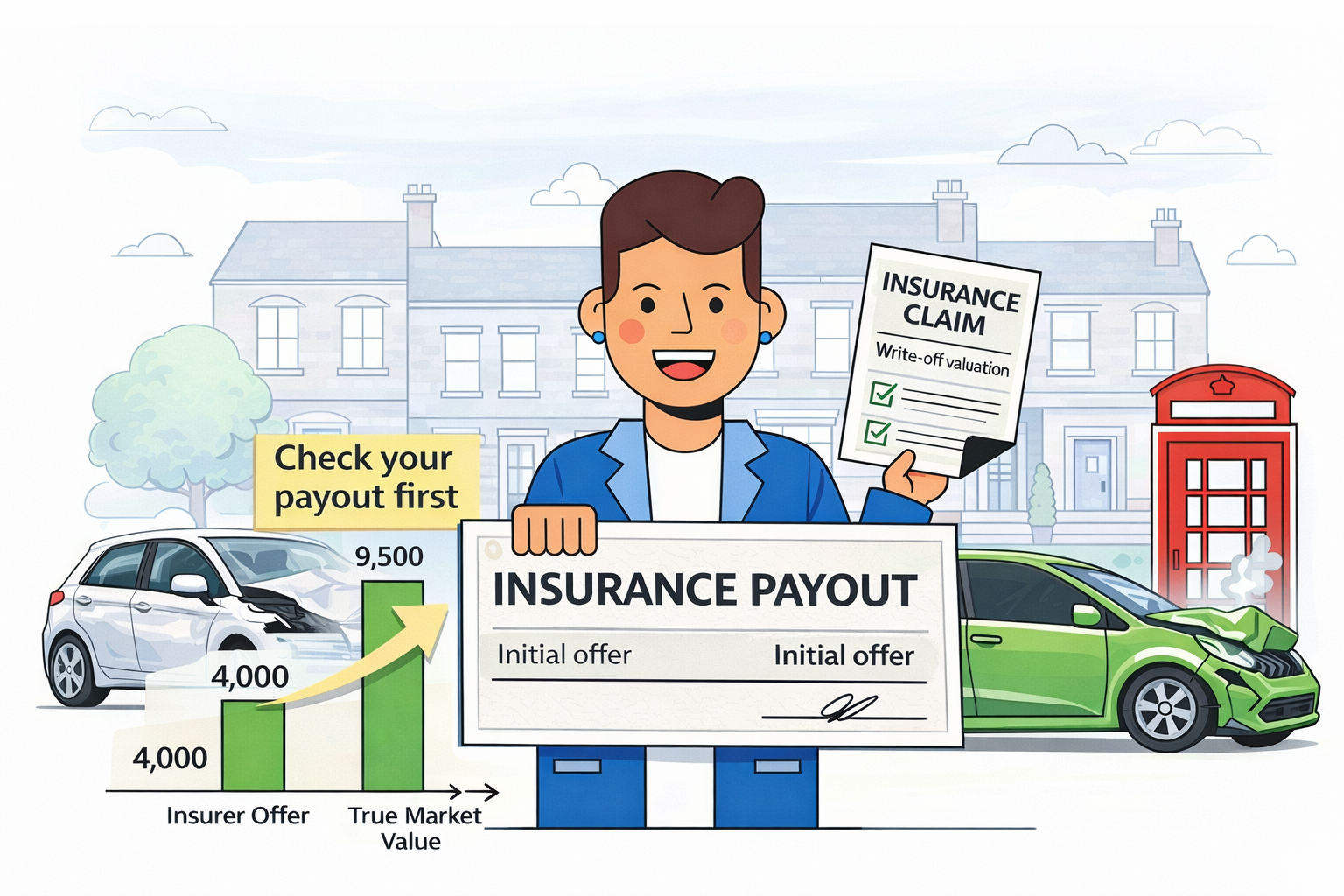

The customer’s car was declared a total loss (write-off) following an incident.

Their insurer made an initial settlement offer based on what they claimed was the vehicle’s market value at the time.

However, the customer believed the payout was too low and did not reflect the true value of their vehicle.

The problem: undervaluation of the vehicle

The dispute centred around one key issue:

👉 The insurer’s valuation was significantly lower than the actual market value.

The customer argued that:

- The insurer relied on limited or incorrect valuation data

- Comparable vehicles used were not truly equivalent

- The payout would not allow them to purchase a similar replacement vehicle

What evidence was considered?

The Financial Ombudsman reviewed:

- Industry valuation guides

- Advertised prices of similar vehicles

- Vehicle condition and specification

- Market conditions at the time of the loss

Importantly, the Ombudsman focuses on what it would cost to replace the vehicle, not just trade values.

The Ombudsman’s decision

The Financial Ombudsman upheld the complaint.

They concluded that:

- The insurer’s valuation was not fair or reasonable

- The evidence showed the vehicle was worth more than the amount offered

- The customer had been financially disadvantaged by the low settlement

The outcome

The insurer was required to:

- Increase the settlement by over £6,000

- Pay the difference to reflect the true market value

- Put the customer back in the position they should have been in

Key takeaway from this case

👉 Insurance valuations are not always final — and they can be challenged successfully.

This case highlights that:

- Insurers can undervalue vehicles

- Initial offers are not always accurate

- Strong evidence can significantly increase payouts

Why this matters for UK drivers

Many drivers accept their payout without questioning it.

But this case shows:

- You could be owed thousands more

- The Financial Ombudsman regularly overturns valuations

- You don’t need to accept the first offer

What should you do if your payout seems too low?

If your car has been written off:

- Compare your payout with similar vehicles on the market

- Gather evidence (AutoTrader listings, condition, service history)

- Raise a complaint with your insurer

- Escalate to the Financial Ombudsman if needed

👉 The process is free, and you don’t need a claims company to do it.

Can you still claim if you already accepted the payout?

Yes — in many cases, you can still challenge a settlement after accepting it, especially if you later realise it was undervalued.

Time limits may apply, so it’s best to act as soon as possible.

Check if you were underpaid

If your car was written off and your payout didn’t feel right, you could still recover the difference.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today

Important note

You can complain directly to your insurer and refer your case to the Financial Ombudsman Service for free.