.svg)

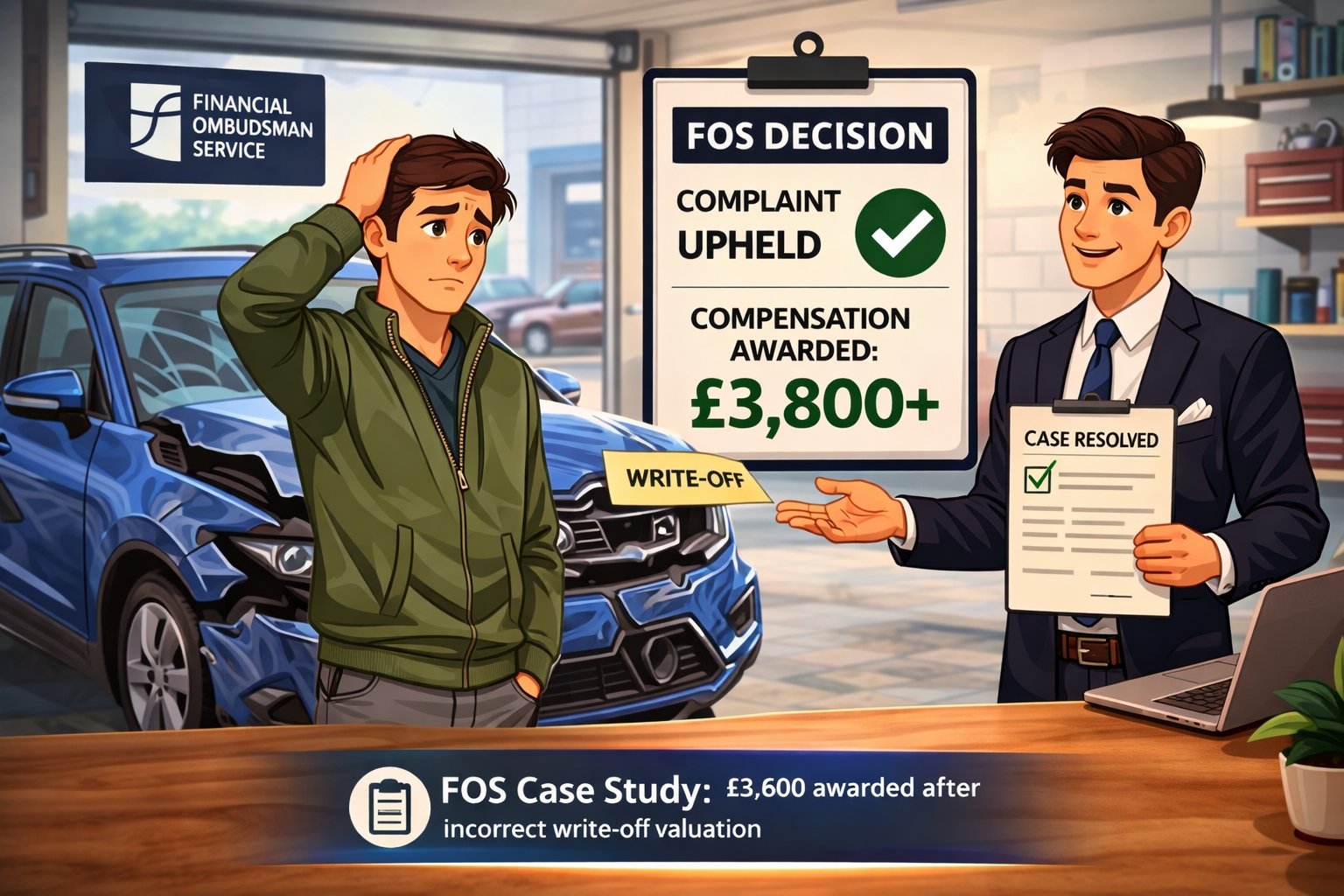

Case Reference: DRN-4721983

Case Type: Vehicle Write-Off / Total Loss

Outcome: Complaint upheld

Additional compensation awarded: £3,800

What happened in this case?

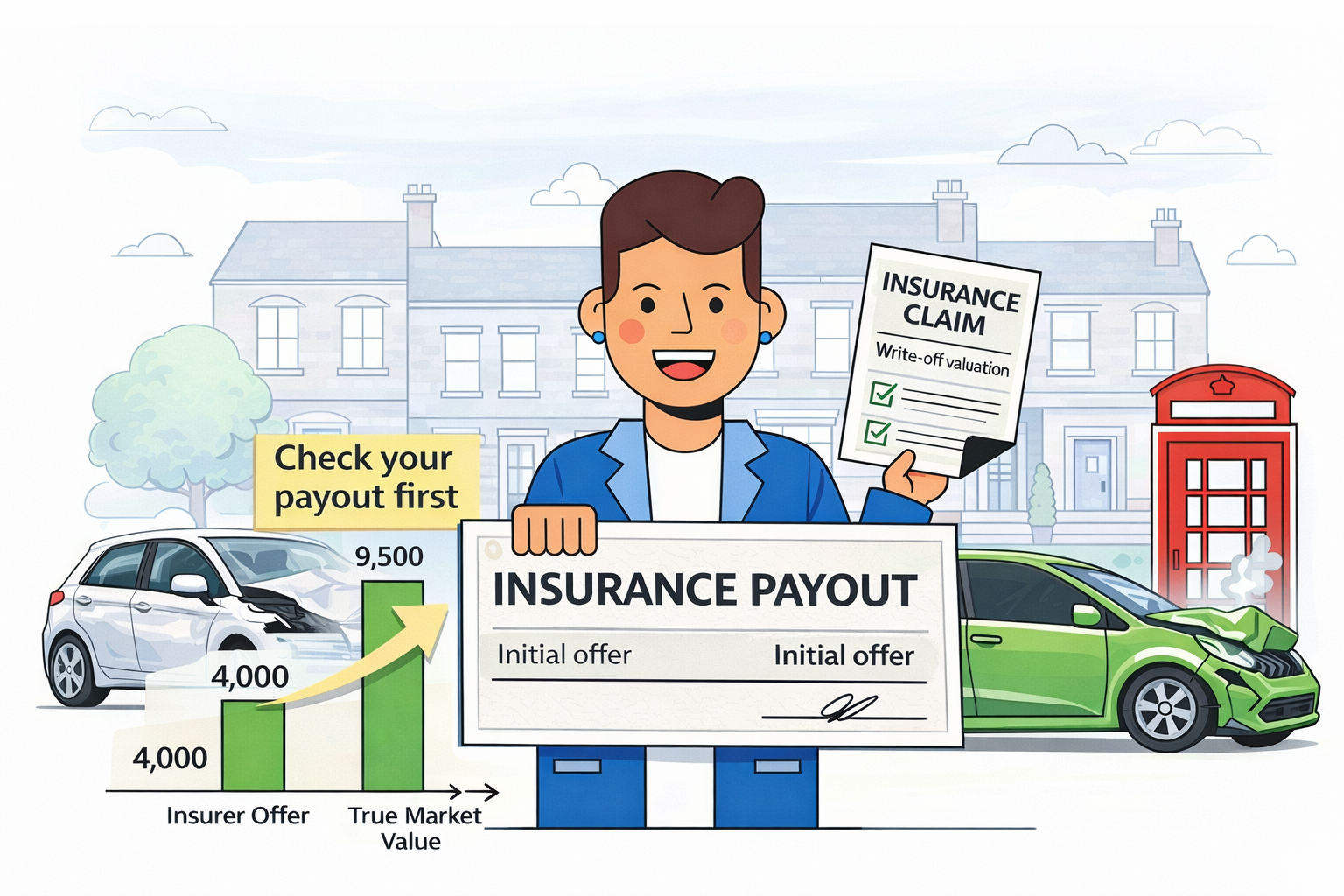

The customer’s vehicle was declared a total loss following an accident.

Their insurer provided a settlement based on its assessment of the car’s market value before the incident.

However, the customer believed the payout was significantly lower than expected, particularly given the vehicle’s condition and specification.

The issue: key vehicle details were overlooked

The dispute arose because the insurer’s valuation did not fully reflect the car’s true value.

The customer argued that:

- The insurer failed to account for optional extras and upgraded features

- The vehicle was in above-average condition

- Comparable vehicles with similar specifications were listed at higher prices

👉 As a result, the settlement did not reflect a like-for-like replacement cost.

What evidence was reviewed?

The Financial Ombudsman reviewed:

- Motor trade valuation guides

- Listings of similar vehicles with matching specifications

- Evidence of optional extras and condition

- The insurer’s valuation methodology

The key consideration was:

👉 Whether the payout fairly reflected the cost of replacing the vehicle with one of similar age, mileage, and specification.

The Ombudsman’s decision

The complaint was upheld.

In case DRN-4721983, the Ombudsman found that:

- The insurer had not fully considered the vehicle’s specification

- The valuation used was too low compared to real market evidence

- A higher payout was necessary to achieve a fair and reasonable outcome

The outcome

The insurer was required to:

- Increase the settlement by £3,800

- Reflect the vehicle’s true market value, including relevant features

- Ensure the customer could reasonably replace their vehicle

Key takeaway from this case

👉 Vehicle specification and condition can significantly impact valuation.

This case highlights:

- Extras and upgrades should be included in valuations

- Not all “standard” valuations are accurate

- Strong evidence can increase payouts by thousands

Why this matters for UK drivers

Many drivers don’t realise their car may be worth more due to:

- Optional extras (e.g. upgraded trim, tech, alloys)

- Excellent condition or full service history

- Desirable specifications in the used market

👉 If these are overlooked, your payout could be significantly undervalued.

What should you do if your car had extras or was in great condition?

If your car was written off:

- List all optional extras and upgrades

- Find similar vehicles with matching specifications

- Gather supporting evidence

- Challenge the insurer’s valuation

- Escalate to the Financial Ombudsman if needed

Do insurers include extras in valuations?

They should — but they don’t always do so correctly.

If key features or condition are ignored, the valuation may not reflect the true market value, giving you grounds to challenge it.

Check if your payout was too low

If your car was written off and your settlement didn’t reflect its true value, you could still recover the difference.

✔ No upfront costs

✔ Quick eligibility check

✔ No Win, No Fee

👉 Start your free check today

Important note

You can complain directly to your insurer and refer your case to the Financial Ombudsman Service for free.